Table of Content

- Options To Lowering Term Life Insurance Coverage

- How To Apply For Decreasing Term Life Insurance

- Waiver Of Premium Cost For Total Incapacity

- Lowering Term Insurance Coverage For Families

- There Are An Quite Lots Of Benefits To Lowering Time Period Life Insurance Coverage These Embrace:

- What's Reducing Term Life Insurance?

You may also wish to think about using each stage term and lowering time period together. For example, you'll be able to choose a $250,000 level time period coverage for 30 years, but add a decreasing time period coverage for 20 years to cover the payoff of your own home and your kids reaching maturity. The coverage kind acknowledges that you may need more protection early within the term than you'll in future years. There are also some disadvantages to a decreasing term life insurance coverage. With reducing term insurance coverage, you might have the security of knowing that your loved ones can repay the mortgage if you die during the term of the policy.

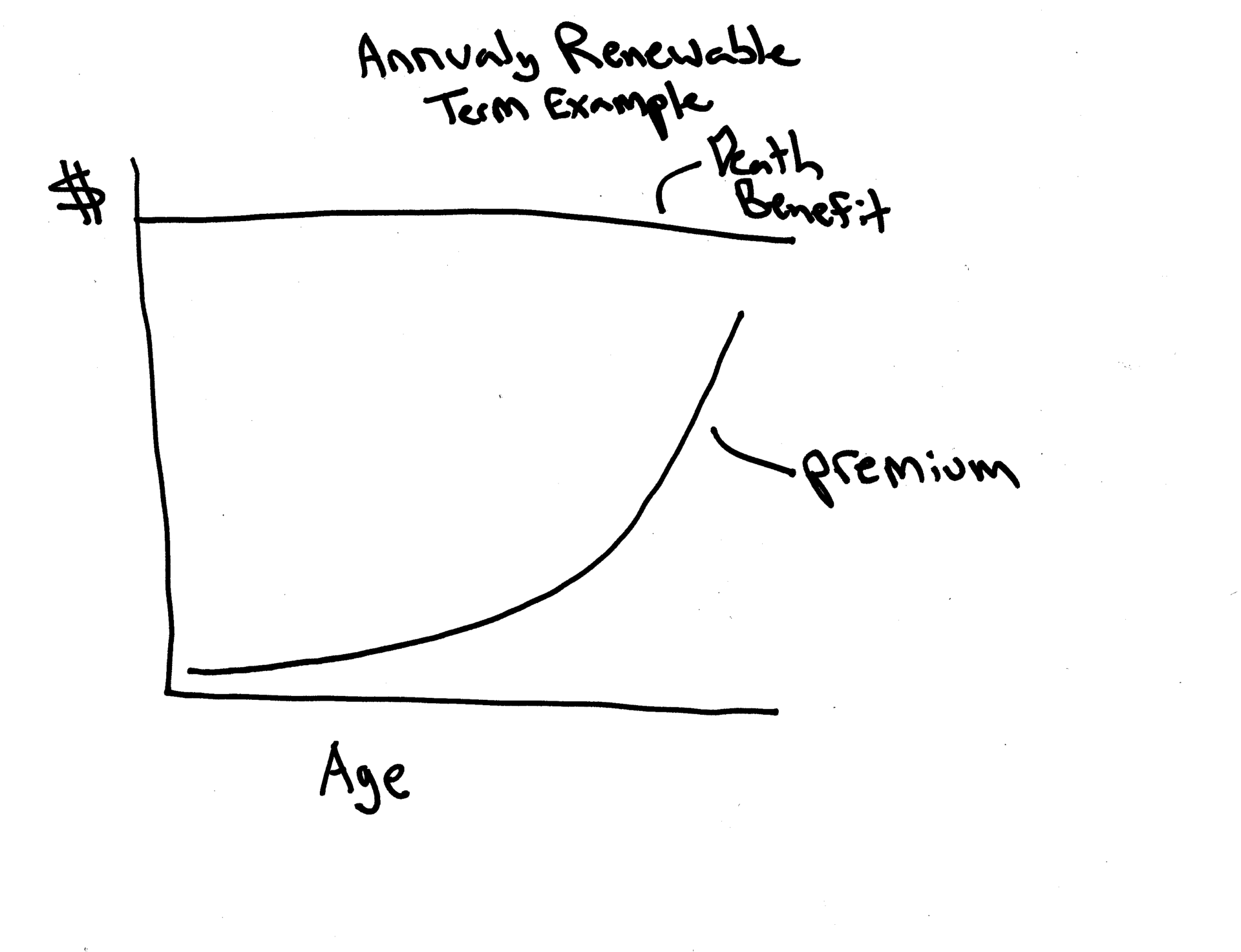

Unlike level term life insurance, which pays out a fixed lump sum of money on the dying of the policyholder, the value of a reducing time period policy reduces over the coverage term. Depending on your mortgage, certain life insurance coverage providers could give you the option of a lowering time period life insurance coverage coverage which supplies extra cowl than your mortgage. This can help your family to cowl further expenses quite than masking only the mortgage if you cross away. Although it might be much like level time period insurance in regard to duration, level term insurance coverage has a set quantity of premium and demise benefits.

Alternate Options To Decreasing Time Period Life Insurance Coverage

To protect yourself financially within the case of great illness, contemplate crucial illness cowl. Decreasing time period life insurance is a kind of life insurance coverage which might present monetary protection for your family should you cross away. This life insurance coverage policy can give you the peace of thoughts that your loved ones will have the funds for to repay a selected outstanding debt, typically a mortgage, within the occasion of your demise. There are some conditions that a reducing term life insurance coverage policy makes sense.

If you might have a reimbursement mortgage, the amount you owe decreases over time as you make monthly repayments. As the excellent mortgage reduces, the value of reducing term insurance goes down. This usually continues till the mortgage is repaid, at which level the value of the quilt is zero. Level time period insurance presents steady premiums and guarantees higher financial safety than reducing time period insurance over a specific length of time . Level term life insurance coverage can be an effective alternative for basic revenue and can cowl giant expenses like funeral prices or well being care payments. When you buy lowering time period life insurance coverage, you choose the extent and length of coverage.

How To Apply For Lowering Time Period Life Insurance Coverage

Our devoted staff will work carefully with you from the beginning till the end, so there’s no need for stress or guesswork when looking for the right life insurance coverage. The least expensive type of everlasting coverage is assured common life or listed common life. These partnerships have formal buy-sell agreements using life insurance coverage to divide the enterprise shares with the untimely death of a associate. The principal, the quantity wanted to pay back the loan, decreases over time as payments are made. While normal stage term policies typically require more medical questions and an examination, together with blood work. Our insurance coverage staff is composed of agents, knowledge analysts, and customers like you.

Decreasing term life insurance coverage can also be a superb nice choice for enterprise homeowners. If you're in a enterprise partnership with unpaid loans and also you die, your business associate takes on your share of the debt. Like individuals with private loans, because the debt is paid off over time, the need of static protection decreases concurrently. Whole life insurance coverage is substantially dearer than time period choices when you evaluate these charges to the time period life rates talked about earlier. So if you’re involved with paying lots in monthly rates, it could be in your finest curiosity to purchase a regular time period policy with a payout that stays level all through your term.

It lasts for a specified period of time, typically ranging from five to 30 years. If you’re on the lookout for life insurance corporations that promote decreasing time period life insurance coverage, you've many high insurance coverage companies to select from. John Hancock, Protective, and plenty of others provide it as a type of term life insurance coverage.

Because of the diminishing dying benefit, lowering time period life insurance coverage could also be cheaper than level term life insurance coverage. Unlike a level term life insurance coverage, the payout or dying benefit of a decreasing time period life policy lessens over time. Decreasing time period life insurance is a term life coverage with a payout that decreases over time.

Lowering Time Period Insurance Coverage For Households

While many Americans are familiar with conventional term and complete life insurance policies, they will not be educated about other options corresponding to lowering time period life insurance. A decreasing-term life insurance policy is an affordable choice for anyone who needs life insurance. If you lately obtained a mortgage, auto, or another sort of mortgage, you might wish to consider buying one. The main function of obtaining time period life insurance is to take care of the financial welfare of the policyholder’s family. Regardless, since the major profit is to make sure the monetary stability of the policyholder and its beneficiaries, it is typically acquired as a outcome of your mortality threat heightens as you age.

According to Business Insider, you would be left with out protection when you pay off your mortgage and wouldn't have other life insurance insurance policies in place. So if you’re looking for the best life insurance firms that pay out, whole life insurance coverage might be your finest option. Level term life insurance is a life insurance coverage policy that guarantees to have the same premium for the entire length of the contract. Many everlasting insurance policies permit policyholders to take a money loan on the protection. The loan quantity that is advanced from the policy will scale back the general dying benefit by that amount.

However, you must significantly contemplate whether or not the payout can be sufficient to benefit your family members after you pass away. A decreasing insurance coverage policy is useful for those who need coverage for a set period of time. It may also be less expensive than level term life insurance coverage insurance policies and let you buy extra coverage. As an example of how reducing time period insurance coverage works, say Bill needs to cowl his mortgage so that his wife, Mary, can maintain the home if he passes away. Bill buys a 30-year reducing time period life insurance policy with a $500,000 dying benefit and lists Mary because the beneficiary. But if he dies within the third year of the coverage, Mary will receive a decreased dying advantage of roughly $466,600.

This is often the largest financial burden confronted by a household and it can be reassuring to know that the mortgage shall be taken care of if the worst happens. Because lowering term insurance policies are oftentimes used for people who want to cover the lowering balance of a mortgage, these policies may be known as mortgage life insurance. You could additionally purchase a time period or whole life policy with a lower dying profit. This would decrease your month-to-month charges whereas still allowing you to have the identical payout at the time of your demise. Your beneficiaries wouldn't have to fret a couple of diminishing payout based mostly on the age of your policy.

The death profit decreases over time with reducing term life insurance. Both term coverage types usually have the same vary of term lengths, which vary from five to 30 years, with some firms providing coverage for forty years. Compared to standard time period and everlasting life insurance coverage, lowering term is usually the least costly.

No comments:

Post a Comment